Does your money seem to disappear each month, leaving you wondering where it all went? If your traditional budget isn’t giving you the financial clarity you need, it might be time for a different approach. Zero Based Budgeting (ZBB) offers a powerful way to take control of your finances by making every dollar work for you.

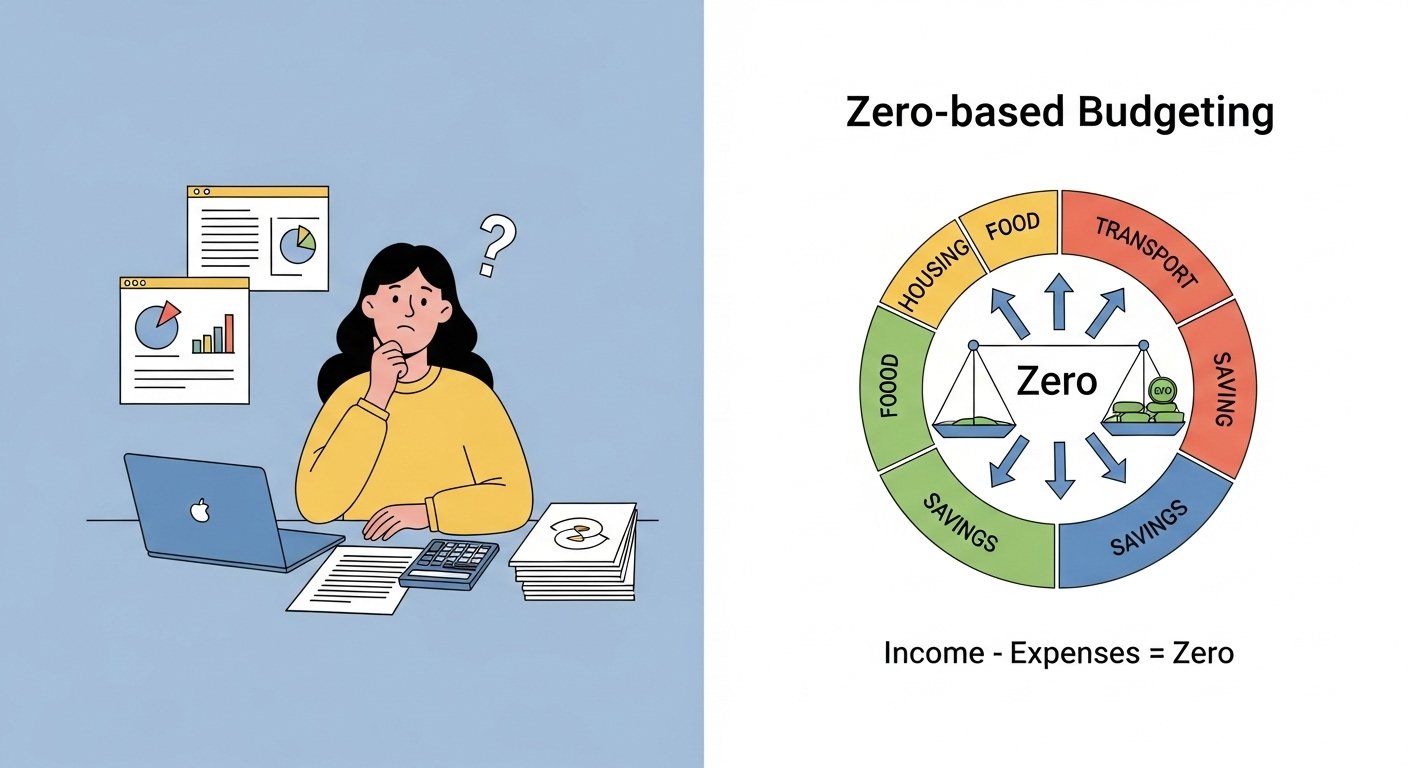

ZBB is a budgeting method where you start from a zero base at the beginning of each new budget period. Instead of carrying over last month’s figures, you justify every single expense. The goal is simple: your income minus your expenses should equal zero. This doesn’t mean you spend everything you earn. It means every dollar is intentionally allocated to an expense, a savings goal, or debt repayment.

This method forces you to be mindful and deliberate with your money. For businesses, it translates to scrutinising every cost to ensure it aligns with strategic goals. For individuals, it’s about building a spending plan that reflects your priorities, whether that’s saving for a house deposit, paying off credit card debt, or planning a dream holiday.

If you’re ready to gain a deeper understanding of your financial habits and make more intentional decisions, this guide will walk you through everything you need to know about implementing Zero Based Budgeting.

How to Implement Zero Based Budgeting Method

Getting started with ZBB involves a few straightforward steps. It requires a bit more effort upfront than traditional budgeting, but the clarity and control you gain are well worth it.

Step 1: Calculate Your Monthly Income

The first step is to figure out exactly how much money you have coming in each month. For those with a fixed salary, this is simple. If your income is variable, for example, if you’re a freelancer, a small business owner, or work on commission, it’s best to use a conservative estimate or an average from the last few months. Tally up all sources of income, including your primary salary, side hustles, and any other regular earnings. This total figure is the starting point for your budget.

Step 2: List All Your Monthly Expenses

Next, create a comprehensive list of all your expenses for the month. Go through your bank statements and credit card bills from the last few months to ensure you don’t miss anything. It’s helpful to categorise your expenses to see where your money is going. Common categories include:

- Housing: Rent or mortgage, rates, utilities (electricity, water, gas).

- Transportation: Car payments, insurance, petrol, public transport.

- Food: Groceries, dining out, coffee.

- Personal: Clothing, toiletries, haircuts.

- Debt Repayment: Credit cards, personal loans, student loans.

- Savings & Investments: Emergency fund, retirement contributions, investment accounts.

- Entertainment: Subscriptions (Netflix, Spotify), hobbies, social outings.

Step 3: Allocate Your Income Until It Reaches Zero

Now for the core of ZBB: assign every dollar of your income to a specific category. The formula is straightforward: Income – Expenses = 0.

Start with your essential, non-negotiable expenses like rent, utilities, and loan repayments. Then, move on to variable spending like groceries and transport. Finally, allocate the remaining funds to your financial goals, such as savings, investments, or extra debt payments, and discretionary spending like entertainment. If you have money left over after allocating to all your needs and wants, direct it towards a savings or investment goal. If you find you have more expenses than income, you’ll need to review your variable spending categories and identify areas where you can cut back.

Step 4: Track Your Spending and Adjust

A budget is only effective if you stick to it. Throughout the month, diligently track your spending to ensure you’re staying within the limits you’ve set for each category. You can use a spreadsheet, a notebook, or a budgeting app to monitor your progress.

Life is unpredictable, so don’t be afraid to adjust your budget if necessary. If an unexpected expense arises, you’ll need to move money from another category to cover it. The key is to remain intentional and make sure your budget still balances to zero at the end of the month.

The Advantages of Zero Based Budgeting Method

Adopting ZBB can have a transformative impact on your financial health. Here are some of the key benefits:

- Complete Financial Awareness: ZBB forces you to examine every expense, which gives you a crystal clear picture of where your money is going. This heightened awareness is the first step toward better financial decision making.

- Improved Cost Control: By justifying each expense, you’re more likely to identify and eliminate wasteful spending. This leads to more efficient use of your resources, whether in a household or a business setting.

- Faster Progress Towards Goals: Because you prioritise allocating funds to savings and debt repayment, you can make more significant and faster progress toward your financial goals.

- Increased Flexibility: A zero based budget is created fresh each month, making it highly adaptable to changes in your income or expenses. This flexibility allows you to respond effectively to financial shifts.

Common Challenges and How to Overcome Them

While ZBB is highly effective, it does come with its challenges. Being aware of them can help you stay on track.

One of the biggest hurdles is the time and effort required, especially when you’re just starting. Tracking every single dollar can feel tedious.

- Solution: Use budgeting apps like Pocketbook or You Need a Budget (YNAB) to automate much of the tracking process. Start simple and add more detail to your budget as you get more comfortable.

Another common issue is dealing with irregular expenses, like annual insurance premiums or car registration.

- Solution: Create dedicated “sinking funds” for these expenses. Each month, set aside a fraction of the total cost (e.g., 1/12th of your annual car insurance premium) so the money is there when the bill is due.

Finally, staying motivated can be tough.

- Solution: Set small, achievable goals and celebrate your wins along the way. Seeing tangible progress—like a growing savings account or a shrinking credit card balance—can be a powerful motivator.

Tools and Resources for Zero Base Budgeting Method

You don’t have to go it alone. There are plenty of tools available to make Zero Based Budgeting easier:

- Spreadsheets: A simple spreadsheet in Google Sheets or Microsoft Excel is a free and customisable way to manage your budget.

- Budgeting Apps: Apps like You Need a Budget (YNAB) are specifically designed for the ZBB method. Other popular apps in Australia include Pocketbook and Frollo.

- Notebook and Pen: For those who prefer a hands-on approach, a dedicated notebook can be just as effective. The physical act of writing down your budget can reinforce your commitment.

Build a Stronger Financial Future

Zero Based Budgeting is more than just a method for tracking money; it’s a mindset that empowers you to be the master of your finances. By assigning a job to every dollar you earn, you ensure that your spending aligns with your values and your goals. While it requires discipline and effort, the financial clarity, control, and confidence you gain are invaluable.

Ready to stop wondering where your money went and start telling it where to go? Give Zero Based Budgeting a try for one month. You might be surprised at what you discover and how quickly you can start making meaningful progress toward the life you want.

Zero Base Budgeting Method FAQ

1. What is Zero Based Budgeting (ZBB)?

Zero Based Budgeting is a financial method where every dollar of your income is assigned a specific purpose, such as expenses, savings, or debt repayment, leaving a balance of zero at the end of your budget. This approach ensures that your spending is intentional and aligned with your financial goals.

2. Do I need to re-create my budget every month?

Yes, ZBB works best when you tailor your budget to each month’s unique expenses. For example, months with holidays, birthdays, or irregular bills (like insurance premiums) may require adjustments to ensure all expenses are accounted for.

3. What happens if I overspend in one category?

Overspending can happen, but the key is to adjust. Use money from another category in your budget to cover the shortfall, then revisit your spending habits to prevent future overspending.

4. Can I still use credit cards with Zero Based Budgeting?

Yes, but it’s important to stay disciplined. Allocate funds in your budget for any credit card spending and pay off the balance in full each month. This ensures you avoid unnecessary debt while still benefiting from any rewards or cashback.

5. How do I handle irregular income with ZBB?

If your income fluctuates, base your budget on your lowest expected monthly income. When you earn more, allocate the extra funds to savings or other priorities in your budget, ensuring you maintain control and flexibility.