Feeling a bit tangled up with your money? You’re not alone. Whether you’re just starting out with grown up finances or you’ve been around the block a few times and want to get a better handle on your super, a personal budget spreadsheet can be an absolute game-changer.

Forget fancy apps and expensive subscriptions, we’re going to show you how to whip up your own, totally free, and perfectly tailored to your life.

Why Budgeting?

Let’s be honest, talking about money can feel a bit like wading through treacle. But here’s the kicker: knowing where your hard earned cash is going is the first step to making it work for you.

Think of your budget as your financial GPS. It shows you where you are, where you want to go, and how to avoid those annoying detours (like impulse buys or unexpected bills).

For us Aussies, understanding your money flow is especially crucial. From navigating superannuation contributions to making sense of HECS-HELP repayments or just trying to save for that dream holiday or a deposit on a place, a clear picture of your finances gives you power.

It’s not about restriction; it’s about freedom and making informed choices.

Getting Started

Before we dive into the spreadsheet nitty-gritty, let’s talk mindset. This isn’t about deprivation. It’s about being mindful and intentional.

- Be Patient: You won’t nail it on day one, and that’s okay. It’s a learning curve.

- Be Realistic: Don’t cut everything out. If you love your weekly smashed avo on toast, factor it in!

- Be Kind to Yourself: Life happens. Some weeks will be better than others. Just get back on the horse.

- Think Long Term: This isn’t just for next month; it’s building habits for your future self, especially when it comes to things like boosting your super or saving for a deposit.

Free Personal Budget Spreadsheet

You don’t need expensive software. Google Sheets or Microsoft Excel will do the trick nicely. We’ll focus on Google Sheets here because it’s free and accessible anywhere with an internet connection.

Step 1: Set Up Your Basic Structure

Open a new, blank Google Sheet. Let’s give it a clear title, like My Awesome Aussie Budge (or whatever month you’re starting).

You’ll want to create a few key columns across the top. Think of it like this:

- Category: This is where you list all your income sources and expenses (e.g., Salary, Rent, Groceries).

- Budgeted Amount ($): This is the amount you plan to earn or spend for each category in a month.

- Actual Amount ($): This is what you actually earned or spent. You’ll fill this in as the month goes on.

- Difference ($): This column will automatically show you if you’re over or under budget for each item.

- Notes: A handy spot for any comments or reminders.

Below these headings, you’ll divide your sheet into three main sections: Income, Expenses, and Savings & Investments.

Within Expenses, it’s good practice to separate Fixed Expenses (things that are usually the same amount each month, like rent) from Variable Expenses (things that change, like groceries or eating out).

Step 2: Understand the Formulas

This is where your spreadsheet does the heavy lifting. You’ll use simple formulas to add up your totals and calculate the Difference.

To get a clear picture of your finances, you’ll need to calculate a few key totals within your spreadsheet. This helps you compare what you planned to spend versus what you actually spent.

First, you’ll want to add up all your income items to get your Total Income. Do this for both your ‘Budgeted’ and ‘Actual’ income columns.

Next, combine all your expense items to arrive at your Total Expenses. Again, calculate this for both your ‘Budgeted’ and ‘Actual’ expense columns.

Once you have your totals, you can figure out your Net Balance. This is simply your Total Income minus your Total Expenses. You’ll do this calculation for both your ‘Budgeted’ and ‘Actual’ columns to see how much you ideally should have left over, and how much you actually did.

Finally, to see how well you stuck to your plan for each individual item, calculate the Difference. For every single income and expense category, subtract your ‘Budgeted’ amount from your ‘Actual’ amount.

If you end up with a positive number, it means you either earned more or spent less than you planned! A negative number indicates you earned less or spent more than expected, showing areas where you might need to adjust your habits or your budget going forward. You can quickly apply this difference calculation to all your categories.

Step 3: Let’s Fill It In With an Example!

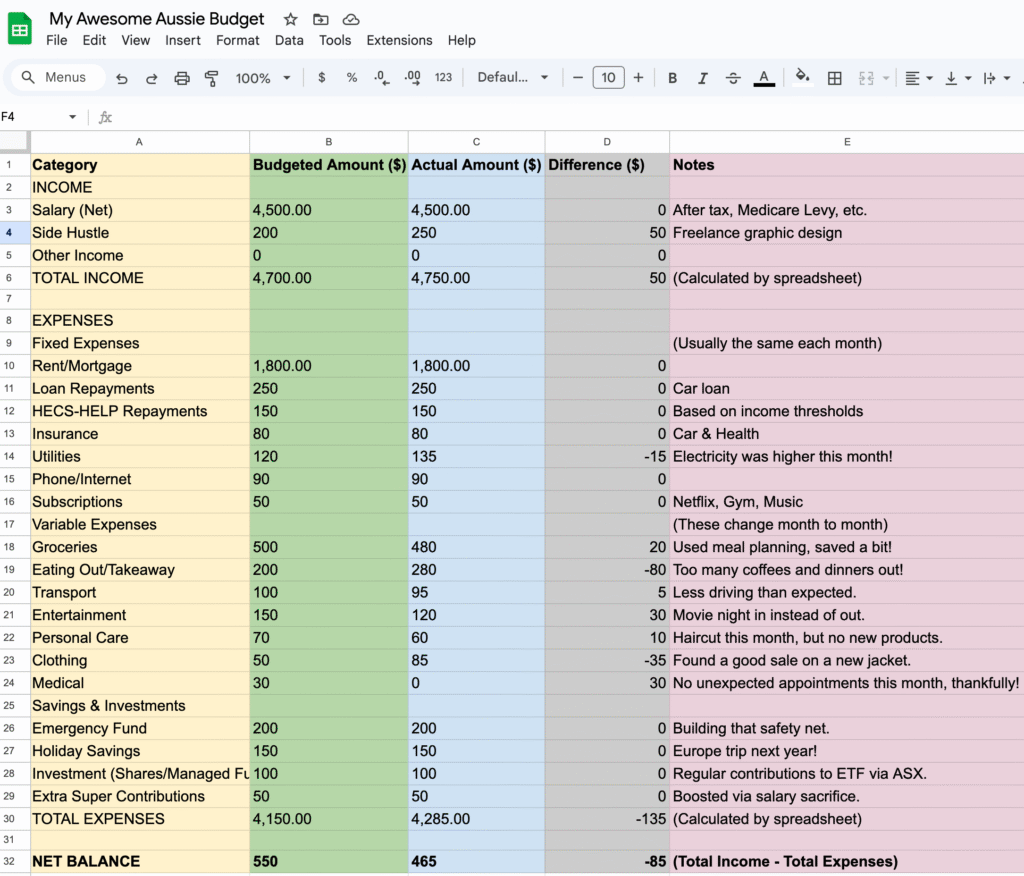

To make this super clear, here’s what your spreadsheet might look like with some example figures for a hypothetical Aussie. Imagine this is for August.

MY AWESOME AUSSIE BUDGET – AUGUST 2025

| Category | Budgeted Amount ($) | Actual Amount ($) | Difference ($) | Notes |

| INCOME | ||||

| Salary (Net) | 4,500.00 | 4,500.00 | 0.00 | After tax, Medicare Levy, etc. |

| Side Hustle | 200.00 | 250.00 | 50.00 | Freelance graphic design |

| Other Income | 0.00 | 0.00 | 0.00 | |

| TOTAL INCOME | 4,700.00 | 4,750.00 | 50.00 | (Calculated by spreadsheet) |

| EXPENSES | ||||

| Fixed Expenses | (Usually the same each month) | |||

| Rent/Mortgage | 1,800.00 | 1,800.00 | 0.00 | |

| Loan Repayments | 250.00 | 250.00 | 0.00 | Car loan |

| HECS-HELP Repayments | 150.00 | 150.00 | 0.00 | Based on income thresholds |

| Insurance | 80.00 | 80.00 | 0.00 | Car & Health |

| Utilities | 120.00 | 135.00 | -15.00 | Electricity was higher this month! |

| Phone/Internet | 90.00 | 90.00 | 0.00 | |

| Subscriptions | 50.00 | 50.00 | 0.00 | Netflix, Gym, Music |

| Variable Expenses | (These change month to month) | |||

| Groceries | 500.00 | 480.00 | 20.00 | Used meal planning, saved a bit! |

| Eating Out/Takeaway | 200.00 | 280.00 | -80.00 | Too many coffees and dinners out! |

| Transport | 100.00 | 95.00 | 5.00 | Less driving than expected. |

| Entertainment | 150.00 | 120.00 | 30.00 | Movie night in instead of out. |

| Personal Care | 70.00 | 60.00 | 10.00 | Haircut this month, but no new products. |

| Clothing | 50.00 | 85.00 | -35.00 | Found a good sale on a new jacket. |

| Medical | 30.00 | 0.00 | 30.00 | No unexpected appointments this month, thankfully! |

| Savings & Investments | ||||

| Emergency Fund | 200.00 | 200.00 | 0.00 | Building that safety net. |

| Holiday Savings | 150.00 | 150.00 | 0.00 | Europe trip next year! |

| Investment (Shares/Managed Funds) | 100.00 | 100.00 | 0.00 | Regular contributions to ETF via ASX. |

| Extra Super Contributions | 50.00 | 50.00 | 0.00 | Boosted via salary sacrifice. |

| TOTAL EXPENSES | 4,150.00 | 4,285.00 | -135.00 | (Calculated by spreadsheet) |

| NET BALANCE | 550.00 | 465.00 | -85.00 | (Total Income – Total Expenses) |

Step 4: Fill in Your Income

This is the fun part! Add up all your regular income after tax, just like it hits your bank account. If you’re employed, this is your net salary. If you’ve got a side hustle or receive benefits, chuck those in too. Be realistic – if your side gig income varies, take an average or be conservative.

- Tip: If you’re salary sacrificing into your super, remember your net salary is what’s left after those contributions.

Step 5: Tackle Your Fixed Expenses

These are the bills that generally stay the same month in, month out. Your rent or mortgage repayments, regular loan payments (like a car loan or even your HECS-HELP contributions if they’re a fixed amount), insurance premiums, and essential subscriptions.

Go through your bank statements for the last few months to get accurate figures.

Step 6: Estimate Your Variable Expenses

This is where many people get tripped up. Variable expenses fluctuate, but with a bit of detective work, you can get pretty close.

- Groceries: Look at your last few months of supermarket spending.

- Eating Out/Takeaway: Be honest with yourself! This can be a big budget buster.

- Transport: Fuel costs, public transport fares.

- Entertainment: That pub feed with mates, movie tickets, concerts.

The best way to get accurate figures is to track your spending for a week or two, then multiply it out. Or, again, go through past bank statements.

Step 7: Don’t Forget Savings & Investments

This is crucial for building wealth in Australia. Think about:

- Emergency Fund: Aim for at least 3-6 months of living expenses in an accessible savings account.

- Specific Goals: Holiday savings, a new car, a house deposit (First Home Super Saver Scheme might be relevant here!).

- Investments: Are you putting money into shares through the ASX, or managed funds?

- Extra Super Contributions: A great way to boost your retirement nest egg and potentially save on tax.

Treat savings as a non-negotiable expense. Pay yourself first!

Tracking Your Spending

Once your spreadsheet is set up, the real work (and payoff!) begins: tracking.

The Actual Amount Column

Throughout the month, as you spend, update the Actual Amount column for each category.

- Daily Check-ins: A quick 5 minute check-in daily can make a huge difference.

- Bank Statement Power: Regularly review your online banking. Many banks (like CommBank, Westpac, NAB, ANZ) categorise transactions for you, which can be a good starting point.

- Receipts: Keep them handy for cash purchases, or snap a photo.

- Apps: While we’re focusing on free spreadsheets, some budgeting apps can link to your bank accounts and automate this tracking, which you can then export to your spreadsheet for a holistic view.

Reviewing the Difference Column

This is where you learn. At the end of the month, look at the Difference column.

- Positive Numbers: Great! You came in under budget or earned more.

- Negative Numbers: This is where you might need to adjust. Did you overspend on dining out? Were utility bills higher than expected? This isn’t about guilt; it’s about understanding and making a plan for next month.

Optimising Your Budget

Once you’ve got a month or two under your belt, you’ll start to see patterns. This is when you can really start to make smart choices.

- The 50/30/20 Rule (Aussie Edition): A good general guideline is:

- 50% Needs: Rent/mortgage, utilities, groceries, transport.

- 30% Wants: Eating out, entertainment, subscriptions, new clothes.

- 20% Savings & Debt Repayment: Emergency fund, investments, extra loan payments, boosting your super.

2. Spotting Savings Opportunities:

- Utilities: Shop around for better electricity or internet deals. There are comparison sites specifically for Australia.

- Insurance: When was the last time you reviewed your car or home and contents insurance? You might be paying for more than you need, or could get a better deal elsewhere.

- Subscriptions: Are you actually using all those streaming services?

- Groceries: Meal planning, buying in bulk, and shopping at different supermarkets can save a bundle.

3. Superannuation Sweet Spots: Your budget can help you identify if you have surplus cash to make voluntary contributions to your super. This can be a savvy tax move and really supercharge your retirement savings over the long term. Chat to your super fund or check the ATO website for contribution limits.

How to fix Common Budgeting Headaches

- I always forget to track: Set a recurring reminder in your phone. Make it a routine, like your morning coffee.

- My income isn’t regular: If you’re a casual worker or self employed, budget based on your lowest expected income, and treat any extra as a bonus for savings or specific goals.

- Unexpected expenses keep popping up: This is exactly why an emergency fund is vital. Factor in a small amount for miscellaneous or buffer each month until your emergency fund is healthy.

- It feels too restrictive: Budgeting is about giving you permission to spend in areas you value, while consciously cutting back on things that aren’t important to you. It’s about freedom, not handcuffs.

Creating a personal budget spreadsheet isn’t just about numbers; it’s about gaining control, reducing stress, and building the financial future you want. It might seem like a bit of effort upfront, but the peace of mind and the clarity it provides are truly priceless.

So, what are you waiting for? Grab a cuppa, open a new Google Sheet, and start mapping out your financial journey today. You’ve got this!